Wednesday February 26, 2025 | VICTORIA, BC

Economic analysis by Mary P Brooke | Island Social Trends

Canada’s economy continues to experience a growing state of uncertainty.

While a certain path is never really known, there are many current factors that force households, small business and investors to think about their options.

- Will tariffs on Canadian exports to the United States still be applied starting March 4 as US President Trump has asserted?

- Will Canadians be able to keep up with the grinding burden of the ever-increasing cost of everything — particularly groceries and housing/renting — while somehow managing to pay down high levels of debt?

- Will governments be able to continue much longer with affordability supports? If the consumer carbon tax is cancelled (by either a new Liberal Prime Minister or a Conservative government under Pierre Poilievre) will affordability payouts still continue for low-income Canadians?

- Will cutbacks of programs and employees be necessary in 2025, especially if government needs to support tariff-impacted sectors?

- Will the 2025 federal election lead to a change in how the government manages the economy? Will a new direction look like investment or cutbacks?

- How low will the value of the Canadian dollar go in 2025 compared to the US dollar?

The interest rate is currently 3.0%:

The Bank of Canada policy interest rate was lowered to 3.0% on January 29, 2025. That was a 0.25% drop, considered fair but cautious.

Now that the economy seems to be heading for certain disruption, the Bank of Canada may wish to consider a 50 basis point drop, bringing the interest rate down to 2.5%.

Had this happened sooner, the economy may have been able to recover sooner. Now it’s too late for a natural positive rebound and lowering the rate ‘dramatically’ seems all but necessary in order to help maintain the confidence of mortgage holders, small businesses, and investors.

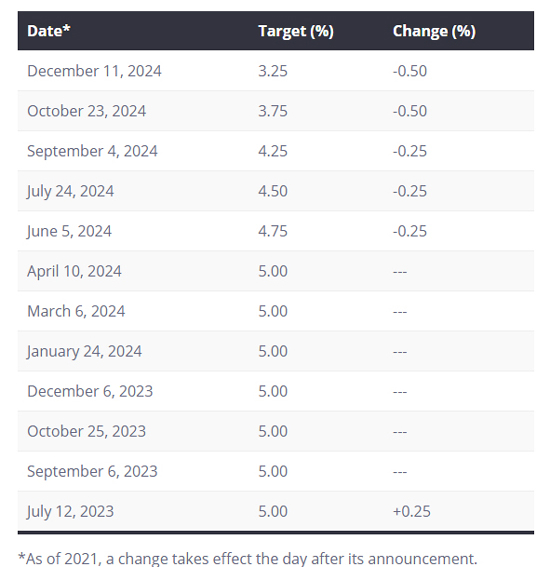

Rates dropped five times in 2024, and again in January 2025:

The Bank of Canada interest rate remained at 5% from July 12, 2023 to June 5, 2024 but then was dropped five times in 2024, landing at 3.25% by year-end:

- On June 5 the rate was lowered by 25 basis points from 5% to 4.75%.

- Then on July 24 the rate was dropped a further 25 basis points to 4.5%.

- On September 4 the rate was dropped another 25 basis points to 4.25%.

- On October 23 the rate was dropped 50 basis points to 3.75%.

- On December 11 the rate was dropped by 50 basis points to 3.25%.

Who benefits by lower rates:

Generally speaking, it is only those who hold mortgages and small business loans and lines of credit at variable rates who will benefit in the short term from any lowering of the central bank’s interest rate.

It is difficult in current economic conditions for businesses to reduce their prices. Even with a drop in interest rates, it’s seen by businesses as more of an opportunity for some modest expense relief as opposed to passing on savings to their customers.

Credit card companies almost never drop their interest rates in any immediate way, if at all, in response to central bank rate cuts. They are still interested in maximum gain from their customers. This is what economists call ‘sticky’ interest rates; once the credit card companies raise their rates they rarely bring them back down, at least not until they’ve had the opportunity to get even more revenue from interest payments by their cardholders.

It seemed odd to hear former finance minister Chrystia Freeland during the Liberal leadership debate on February 25 that she would lower credit card interest rates — a long stretch of a promise at best.

Household debt is now the highest it’s ever been in Canada. This is not about frivolous overspending but in most cases about people relying on credit cards to pay for necessities like groceries, regular family expenses and topping up rent payments. It’s for the most part unsustainable, as many Canadians barely hang on living month to month.

High inflation impacts are embedded:

The impact of high inflation from the post-pandemic period is now fully baked into the cost of nearly everything.

As stated several times by Island Social Trends in recent months — the lowering of the Bank of Canada interest rate has been too slow and too little to really help average Canadians and small businesses.

- People have had to make significant and often long-term adjustments to their lives and lifestyles including paying much higher rents or shifting their household social situation.

- In order to make ends meet many households and small businesses have taken on even more debt (where banks are willing), and/or make smaller less frequent payments on their credit obligations.

- The cost of nearly everything has gone up, including the basics of life like groceries, housing, transportation and insurance.

The spillover effect of those new burdens is seen across society including the impacts on health and well-being of individuals, households and communities.

While everyone focuses on the Bank of Canada when it comes to interest rates, there may need to be a political influence or solution during these extraordinary times of economic warfare imposed by the United States.

Rate announcement dates in 2025:

The Bank of Canada 2025 schedule for policy interest rate announcements includes eight announcement dates:

- Wednesday, January 29 (lowered by 25 basis points to 3.0%)

- Wednesday, March 12

- Wednesday, April 16

- Wednesday, June 4

- Wednesday, July 30

- Wednesday, September 17

- Wednesday, October 29

- Wednesday, December 10

Rates are announced at 9:45 am Eastern Time (6:45 am Pacific). Rates come into effect the day after the announcement.

The Monetary Policy Report will be published concurrently with the January, April, July and October rate announcements.

===== RELATED:

- Jan 29: Bank of Canada drops interest rate to 3.0% (January 29, 2025)

- Significant interest rate drop needed on Jan 29 (January 6, 2025)

- Premier Eby says Bank of Canada interest rate decisions have hurt the BC economy (December 12, 2024)

- Bank of Canada drops interest rate to 3.25% (December 11, 2024)

- Bank of Canada – webcast of December 11, 2024 rate announcement (December 11, 2024)

- Last interest rate announcement of 2024 coming up December 11 (December 4, 2024)

- Canada’s Premiers discuss border & tariffs with Trudeau (November 27, 2024)

- GST winter tax holiday misses political mark, frustrates businesses, and fails many families (November 23, 2024)

- Bank of Canada half-point interest rate drop (October 23, 2024)

- Bank of Canada lowers interest rate to 4.25% (September 4, 2024)

- Bank of Canada drops interest rate for 2nd time in 2024 (July 24, 2024)

- Eby continues to target Bank of Canada about interest rates (July 17, 2024)

- First Bank of Canada rate drop in four years (June 5, 2024)

- NEWS SECTIONS: BUSINESS & ECONOMY | POLITICS | CANADIAN FEDERAL ELECTION 2025 | CANADA-USA